How to Fix Your Credit Score: A Step-by-Step Guide to Boosting Your Financial Health

Your credit score isn’t set in stone - it’s a reflection of your financial habits. With the right steps, you can rebuild, improve, and take control of your financial future.

What is a Credit Score?

A credit score is a numerical representation of your creditworthiness, typically ranging from 0 to 1,200 in Australia. It is calculated based on factors such as:

- Payment History – Have you made repayments on time?

- Credit Utilisation – How much of your available credit are you using?

- Credit Enquiries – How often do you apply for credit?

- Credit Age – How long have you had active credit accounts?

- Defaults & Negative Listings – Have you missed payments or defaulted on a loan?

Different credit reporting agencies (Equifax, Experian, and Illion) may have slightly different scores, but the key principles remain the same.

What is a Good Credit Score in Australia?

Your credit score falls into a range that determines how lenders assess your risk level.

| Credit Score Range | Risk Level | Likliehood of Loan Approval |

|---|---|---|

| 0 - 549 | Poor | Low |

| 550 - 624 | Fair | Moderate |

| 625 - 699 | Good | High |

| 700 - 799 | Very Good | Very High |

| 800+ | Excellent | Excellent |

How to Fix Your Credit Score

Step 1: Check Your Credit Report

Before you can fix your credit score, you need to know what’s in your report. You can request a free copy of your credit report from:

Look for errors, such as incorrect defaults, duplicate accounts, or fraudulent activity. If you find any mistakes, contact the credit reporting agency to dispute them.

Step 2: Pay Off Outstanding Debts

- Prioritise paying overdue accounts and outstanding defaults.

- If you can’t pay in full, contact creditors to set up a repayment plan.

- Avoid late payments—set up direct debits to ensure bills are paid on time.

Step 3: Reduce Your Credit Utilisation

- Aim to keep your credit utilisation below

30% of your total credit limit.

- If you have multiple credit cards, consider consolidating them into a lower-interest loan.

Step 4: Limit New Credit Applications

- Only apply for credit when necessary.

- Every time you apply for credit, a hard enquiry is recorded on your report. Too many applications in a short period can lower your score.

Step 5: Build a Positive Credit History

- Keep your oldest credit accounts open if they are in good standing.

- Use credit responsibly and make small purchases that you repay in full each month.

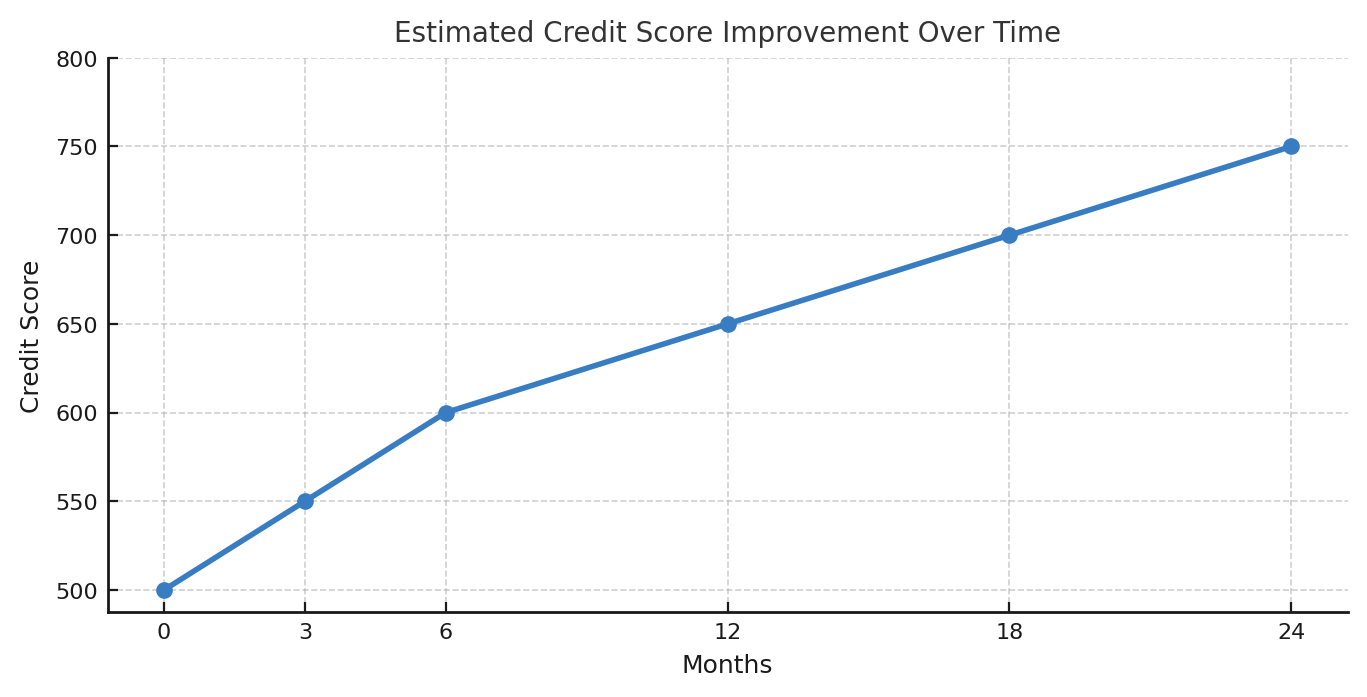

How Long Does It Take to Improve Your Credit Score?

Fixing your credit score takes time and consistency. Below is an estimated timeline of how long it typically takes to see improvements based on different actions:

Estimated Timeline for Credit Score Improvement

| Action Taken | Expected Time for Score Improvement |

|---|---|

| Correcting Credit Report Errors | 1-3 Months |

| Paying Off Outstanding Defaults | 6-12 Months |

| Reducing Credit Utilisation | 3-6 Months |

| Avoiding New Credit Applications | 6-12 Months |

| Maintaining On-Time Payments | 12-24 Months |

Estimated Credit Score Improvement Over Time

Frequently Asked Questions (FAQs)

Can I Fix My Credit Score Fast?

There are no instant fixes, but correcting errors and paying overdue accounts can lead to noticeable improvements within a few months.

Will Paying Off a Loan Increase My Credit Score?

It depends. Paying off a loan can help by reducing debt, but it may also lower your average credit age. Keeping an active, well-managed credit account is beneficial.

Do Late Payments Affect My Score?

Yes, even a single late payment can negatively impact your credit score. Try to automate payments to avoid missing due dates.

Does Checking My Credit Score Lower It?

No, checking your own credit score (a "soft enquiry") does not affect your credit rating. Only formal credit applications (hard enquiries) impact your score.

Final Thoughts

Improving your credit score takes time, but by following these steps—checking your report, paying off debts, reducing credit usage, and building a positive history—you’ll be on your way to better financial opportunities.

If you’re planning to apply for a car loan, fixing your credit score now can help you

secure

lower interest rates and better loan terms.

This tool can quickly estimate how much you can borrow for a car loan. By entering your credit score, monthly payment budget, and loan term, it calculates an estimated loan amount using standard industry practices.

Disclaimer: The results provided by this Car Loan Borrowing Capacity Calculator are for informational purposes only and serve as a general guide. The tool does not take into account all factors that may influence your actual borrowing capacity, such as your debt-to-income ratio, existing financial obligations, lender-specific requirements, or other personal financial circumstances.

The actual loan amount you may qualify for can vary based on the lender’s criteria and other factors that may not be considered here. Always consult with a financial advisor or lender for more accurate and personalized loan advice.